A report into fintech trends last month by McKinsey – Synergy and disruption: Ten trends shaping fintech – caught my attention on the train this morning. Its a good read with some fascinating information, so i thought i would share my quick notes.

What is Fintech?

- McKinsey describe fintech as the fusion of finance and technology resulting in “..the collision of two worlds – and the evolution of the use of technology in financial services”

- With this “collision” comes a union of financial services and technology which brings about both “disruption and synergies” – the key recurring theme in the report

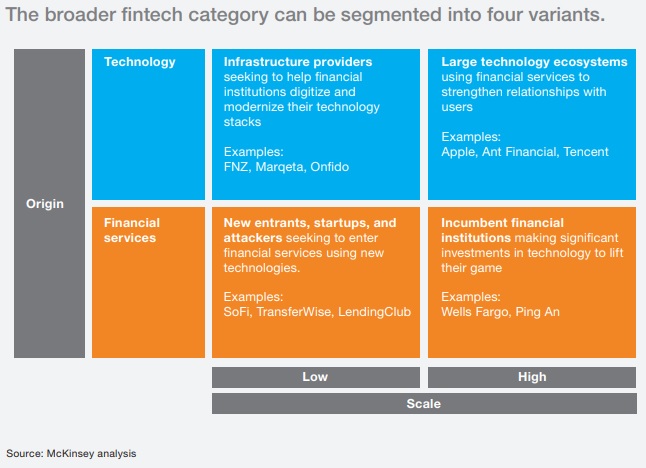

- McKinsey organised Fintech into 4 key but distinct areas:

- Fintechs as new entrants, startups and attackers

- Fintechs as incumbent financial institutions

- Fintechs as ecosystems coordinated by large tech-companies

- Fintech as infrastructure providers

Some stats:

- McKinsey Panorama report that almost 80% of financial institutions have established a fintech partnership

- CB Insights data reveals how global venture capital (VC) fintech investments in 2018 were up to $30.8 billion, compared with $1.8 billion in 2011

1. Significant Regional Differences in Fintech Disruption

McKinsey suggest most of the fintech gains are happening at a regional level, rather than at a global level. Key reason for this is regulation – country and regional based regulation is driving the success of some fintech companies, those that understand and can deal with and manage regulation are winning within their region, and with maturity are eyeing up international expansion plans.

2. AI is an Evolution, not a Revolution for Fintechs

McKinsey highlight given the hype around artificial intelligence (AI) in fintech, there are few successfully scaled and monetised examples. Rather we have the implementation of machine learning coupled with traditional analytics in fintech, and this is why McKinsey feel there will not be a great AI leap forward – rather an evolution into new data sources and methods.

3. Good Execution + Strong Business Model > Bleeding Edge Tech

In short, cutting edge technology alone is not the answer for fintechs. It is about being able to quickly deliver innovative products, good marketing and data driven iterative product and user experience improvements

4. Selective Funding is driving Critical examination of the Business Fundamentals

Even though funding is at an all time high, investors are increasingly selective about where they are putting their investments. There is a move towards later stage fintech companies with a proven track record and signs of scalability and profits.

5. User Experience alone is not enough

As incumbent financial institutions have caught up with innovative fintechs and built a good user experience, McKinsey suggest that “Great UX is now the norm”. As a result, fintechs need to find other ways to sway the customer.

6. Incumbents can, and are, fighting back

Initially incumbent financial institutions were slow to respond to the fintech threat, perhaps fearing self-cannibalisation – now many incumbents are starting to develop their own and/or partner with fintechs to offer digital products. McKinsey cite the Goldman Sachs digital bank Marcus, which signed up 100,000 customers in just over a month

7. Attackers and Incumbents are Joining Forces

Increasing number of incumbents and fintech companies are recognising the value of their combined strengths. In order to grow their business, fintechs are looking for partnerships.

Fintech strengths:

- Fast product development

- Greater risk tolerance

- Flexible to adapt to customer/market changes

Incumbent institution strengths:

- Large number of customers acquired over a long period of time

- Compliance and regulatory capabilities

- Customer trust

8. Infrastructure Fintechs – Have Great Potential but Sales Cycles are Long

Digital innovation within a incumbent banks’ core systems is a risky and complicated venture. Some Core Banking System (CBS) fintechs have emerged, and rather than disrupting incumbents they are looking to partner with financial institutions and upgrade their tech infrastructure enabling a modern, modular, open API environment. But this is a tricky market to get into for fintech companies.

9. Some Fintech’s are Hesitatingly going Public

McKinsey believe there has been a recent mood change (e.g Adyen listing in June 2018 and its share price doubled) with recent fintech listings on various exchanges. This is a key decision that fintechs need to make going forward.

10. Chinese Fintechs have Scaled and Innovated Faster than those in the West

In the west fintech companies have focused on and expanded functionality in one key area (for example payments) and then looked to expand the product to new geographies. In China it has been the big-tech companies that have created financial ecosystems on their existing high-engagement platforms – for example, Alibaba’s e-commerce platform was enhanced to enable online payments using Alipay.