Payments in the UK are changing and a couple of months ago Payments UK released a report – Changing Payments Landscape: How 2017 will change the way we pay for good – outlining the reasons why. The UK payments industry is often described as a global leader paving the way for other countries, innovating and delivering world class payments from Chip and PIN (2003), contactless payments to Faster Payments (2008) – and that together with details of all the different groups and initiatives makes this report pretty interesting. In this post, i summarise the key points:

UK Payments:

1. Customer demands and expectations

The ease, speed and convenience of online shopping has changed customer expectations, and now people want and expect instant frictionless payments

2. New Technology

New tech together with the adaptation of existing tech has instigated new payment methods – for example, the mobile phone evolved into a smartphone with a multitude of apps

3. Competition and Collaboration

Competition –

- Payment service providers must compete with one another to provide better products and improved services to their customers

- New entrants – fintech companies – are innovating in an unprecedented manner to break into and gain market share

Collaboration –

- Some industry wide initiatives (such as contactless payments and faster payments) are driving collaboration within the industry

4. Upgrading Traditional Payment Methods

Alongside all of the exciting payment innovations there is a need to maintain and enhance traditional payment methods too – for example:

- Cheque imaging will speed up cheque clearing

- Polymer banknotes – which include the recently introduced £5 – ensure that the cash notes are cleaner, more secure and durable than the older notes

5. Regulation

Regulation is always mentioned at some point, eh? The objective being to:

- Encourage innovation

- Protect customers

- Enhance competition in the market

6. New Payment Service Providers

Payments UK reports that their are over 2500 payment service providers in the UK, each competing to showcase and offer their own payment services and products

7. The Growth of Online & Mobile Banking

Faster Payments launched in 2008 has laid the foundation for near instant payments, and this Payments UK believe has resulted in the rise and rise of online and mobile banking. This service has evolved with Paym – allowing customers to pay using a smartphone and a recipients telephone number

8. The Rise of Debit Card and Contactless Payments

- Debit card payments have more than doubled from 4 billion payments in 2005 to 10 billion payments in 2015

- Contactless payments since their introduction in 2007 have gone from strength to strength

9. Other Payment Methods have Evolved

While debit cards and contactless payments are becoming more and more popular, their is recognition that traditional payment methods such as cheques (half a billion cheque written in 2015) and cash (in 2015, cash was used for 45% of all payments) are still very important

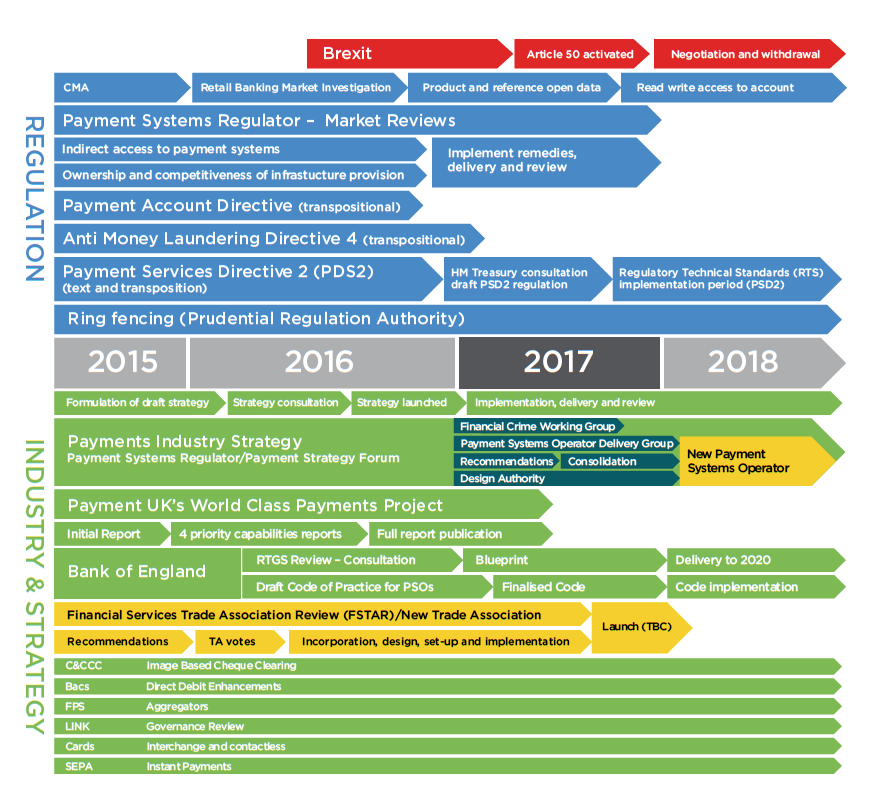

10. Payments Systems Regulator (PSR) and Payments Strategy Forum (PSF)

- 2015 – PSR was established to regulate the payments industry, bring about innovation, encourage innovation and protect and listen to customers

- October 2015 – PSR creates the PSF (industry group) to guide the future of payments in the UK, and initiate projects for the payments industry

11. Payment System Operators (PSO)

The Payment System Operator (PSO) will be a single group made up of BACS, the Cheque and Credit Clearing Company and Faster Payments, and their mandate is to develop payments recommendations by the end of March 2017

12. Open Banking

The Competition and Markets Authority (CMA) in August 2016 recommended that Open Banking standard is implemented which will:

- Give customers greater information and control over their data

- Enable consumers to easily compare similar products

- Allow customer to easily switch providers

Payments in Europe

I hear you say, with Brexit looming any EU payments related laws are not applicable in the UK. Well, that is not true. Until Brexit happens most of the financial regulation within the UK is based on EU law and will remain so until the UK Government and Parliament change it. After Brexit, who know what will happen. But i am guessing that financial services, where possible, will want to continue to retain close ties with Europe and ensure good interoperability.

13. Payments Services Directive (PSD2) and Regulatory Technical Standards (RTS)

- PSD2 intends to promote competition, enable new payment methods, increase customer security and enable wider access to customer data (where permission is given!)

- RTS are being drafted by the European Banking Authority (EBA) to enable strong customer authentication and secure communication

14. Single Euro Payments Area (SEPA)

Yeah….! We know all about SEPA of course, but the initiative has moved on with the Euro Retail Payments Board (ERPB) inviting the European Payments Council (EPC) to create a pan-European euro instant payments scheme.

The SEPA Instance Credit Transfer scheme (SCT Inst) will:

- Enable instant euro credit transfers across 34 European countries

- Allow 24/7 payments up to €15,000

- Ensure payments in less than 10 seconds

- Go live in November 2017

15. Data Protection

From May 2018 the European Commission’s EU Data Protection Reform will aim to protect and respect the privacy/personal data of EU citizens in an increasingly digital world. To ensure compliance payments service providers will need to change the way they handle personal data across the EU

16. Anti-Money Laundering (AML)

The objective of the Fourth Anti-Money Laundering Package is to combat money laundering from criminal activities, prevent the financing of terrorist groups and provide guidelines for the use of virtual currencies.

Payments Industry

17. World Class Payments

Payments UK has established a World Class Payments initiative that will assess and look forward to understand what is needed for the payments systems of tomorrow. This resulted in the development of 13 core payment capabilities – you can read more about these in the post: 12 Payments Trends from Payments UK Worth Reading

18. Confirmation of Payee

Payments UK has recently been working on the Confirmation of Payee (CoP) solution to assess how the payments industry can implement a secure and trusted process to validate the recipients of a payment. The idea here is to ensure that payments are not sent to the wrong recipient/account and to help combat fraudulent payments

19. Standards Collaboration Framework (SCF)

In March 2016 Payments UK founded the SCF to:

- Ensure consistency across the payments industry

- Create a technical repository of UK standards

- Facilitate the creation of common standards within the payments industry

The underlying goal is to ensure that players in the payments space can connect and interact in a common way

20. PSD2 Stakeholder Groups

The Competition and Markets Authority released a report on the Retail Banking Market Review that called upon the Open Banking standard to be PSD2-enabled. This led to the creation of the PSD2 Stakeholder Group which aims to align the implementation of the Open Banking standard with that of PSD2.