Last week the Bank of England Governor. Mark Carney, talked to some students at Edinburgh University about the Future of Money. The speech hit the headlines last week because Mark describing cryptocurrencies as a failure, that needed to be regulated. Its investors were described as fools, while at the same time Mark Carney recognised the benefits of innovative underlying technology. Its pretty hard hitting stuff, so i thought I’d take a deeper look at what exactly was was said. You can see the speech here, or review my recap below.

1. What is Money?

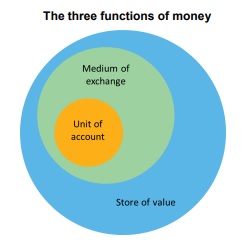

To answer this Mark referenced Adam Smith in The Wealth of Nations, which describes money as:

- A store of value – something that will ideally increase in value in the future

- A medium of exchange – something that enables payments for goods and services

- A unit of account – something that allows you to measure the value of a good, service, saving or loan

With this in mind, Mark explains that money is a social convention – “We accept that a token has value whether made of metal, polymer or code because we expect that others will also do so readily and easily“.

Source: Bank of England – The Future of Money – Speech by Mark Carney

These tokens have changed over time.

2. The Origins of the Bank of England

The Bank of England was founded in 1694 by William Paterson (a Scot) to “promote the good of people” by:

- Issuing hand written bank notes

- Ensuring the bank notes were backed by and exchangeable into gold

- Although this conversion to gold was later suspended as the banks reserve ran low

- Helping to fund King William III’s war with France

The 1844 Bank Charter Act led to the Bank of England being the only bank that could issue notes in England and Wales.

3. The Role of Central Banks

When it comes to money, through history governments and leaders have let their citizens down by devaluing the currency. As a result, many countries have sought to protect the public by creating:

- Centralised, public fiat money

- Robust institutions that oversee money

- Money that is trusted and easy to use

Money is linked by retail and wholesale payment systems, which are intricately linked and critical to the strength of the overall system:

- Banknotes issued by central banks

- Electronic central bank money

- Electronic deposits – created by commercial banks when they offer loans to customers – this constitutes about 80% of money in the system

Central banks have an obligation to ensure appropriate competition, regulation, protection of bank notes from fraud, creation of payment systems, introduction of monetary policy supporting the integrity of the financial system. Mark Carney shared that this comprehensive framework makes it very difficult for other forms of money to compete with sterling (in the UK), enter virtual or ‘crypto’ currencies…

4. The Origins of Cryptocurrencies

Cryptocurrencies came about following the:

- Global financial crisis

- Technological developments

- Dwindling confidence in some bank systems

Mark highlighted the following reasons why cryptocurrencies are more trusted than fiat currencies:

- Cryptocurrency supply is fixed and the value of it cannot be prone to debasement

- Cryptocurrency use is not tied to risky private banks

- Cryptocurrency holders are anonymous, from from prying eyes of tax and law enforcement bodies

- The underlying distributed ledger technology enables payments to be made directly between payer and payee – eliminating the need for intermediaries such as central banks and financial institutions

5. Cryptocurrencies are FAILING – Duh, Duh, Duh..!

Mark Carney believes that cryptocurrencies are failing to act as an alternative form of money, working for only some people. Mark continues to state the following reasons:

Poor Stores of Money – i.e. Cryptocurrencies ain’t stable

- Stating that cryptocurrencies are a “lottery”, sometimes its up other times is down – over the last 5 years, the daily standard deviation of Bitcoin was ten times that of sterling, add to that Bitcoin is probably the most stable cryptocurrency

- Volatility concerns plus “cryptocurrencies have neither intrinsic value nor any external backing”

- Cryptocurrencies show the classic signs of a bubble – bolstered by discussions about new paradigms, retail enthusiasm and crazy price expectations

- The fixed number of Bitcoins is highlighted as a weakness, not a strength, likening it to the creation of the virtual global gold standard

Inefficient Media of Exchange – i.e. Cryptocurrencies ain’t widely accepted

The main reason stated by Mark to be wary of cryptocurrencies is that over the long term value there is uncertainty whether they will become successful media of exchange arguing:

- Right now, no large high street or online retailers accept Bitcoin as valid payment methods in the UK, while “only a handful of the top 500 US retailers do”

- Where cryptocurrencies are accepted, transactions speed and costs vary – proposing that they are “generally slower and more expensive than payments in sterling” – giving the examples that:

- Visa can globally process up to 65,000 transactions per second compared with Bitcoin managing 7 per second

- Debit/credit card transactions take seconds, compared with hours for some Bitcoin transactions

- Bitcoin fees vary £40 in late 2017,and are currently about £2 – compared with retailer costs for cash (1.5 pence), card (8 pence) or online payments (19 pence)

- Bitcoin mining costs are “enormous”, with the current Bitcoin electricity consumption being double that of the electricity consumption of Scotland

- Noting that the global Visa card network half of 1% of that of Bitcoin, while at the same time handling 9000 more transactions

Virtually non-Existent Units of Account – i.e. Traditional currencies provide the benchmark

Mark reiterates the above points that cryptocurrencies are not a good store of value and a unreliable media of exchange and therefore had very little knowledge / evidence of cryptocurrencies being used as units of account

6. The Bank of England Response to Cryptocurrencies or rather Crypto-Assets

- Since cryptocurrencies are not true currencies, in Mark’s opinion, he refers to them as crypto-assets

- Mark believes cryptocurrencies are of increasing interest to policymakers and regardless of their future believes authorities must not inhibit innovation which could ultimately improve financial stability, enable innovation, efficiencies and better payment services

- He also recognises the concerns around consumer and investor protection, market integrity, money laundering, terrorism financing, tax evasion, and the circumvention of capital controls and international sanctions

- Overall, Mark doesnt believe crypto-assets present a material risk to financial stability

Banning Cryptocurrencies

Mark disagrees with the stance taken in China to ban cryptocurrencies (by bannign exchanges, financial institutions and paym using them), highlighting that this halts the potential opportunities presented by the underlying payment technologies

Regulating Cryptocurrencies

This is the option favoured by Mark and the Bank of England, indicating that the crypto-asset ecosystem should be held to the same standards as the rest of the financial system. Enjoying the privileges and the responsibility. As a result authorities in the EU and US are requiring crypto-exchanges to obide by the same level of rules and regulations as financial institutions.

7. The Future of Money

Mark candidly shares that he does not see crypto-assets as the future of money, but accepts that the core technology is important. In fact, Mark points to 3 factors that he believes show that crypto-assets point to the future:

- Money and payments need to meet customer demands and expectations, particularly for instant, direct, decentralised peer to peer networks

- The underlying, particularly distributed ledger, technologies could transform the efficiency, reliability and flexibility of payments

- Bring to the fore questions about whether central banks should provide a Central Bank Digital Currency (CBDC)

Good explanation of Carney’s argument.

I disagree with his costs of transactions – cash has a lot more fixed costs, cards are rarely that cheap for retailers and online payments are typically 1-10p (except for immediate payments or RTGS).